Jul 18, 2025

Beginner's Guide to Filing a Motorcycle Insurance Claim: Step-by-Step Process for New Riders

Beginner's Guide to Filing a Motorcycle Insurance Claim: Step-by-Step Process for New Riders

Master motorcycle insurance claims with our step-by-step guide. Learn documentation tips, avoid costly mistakes, and get back on the road faster.

Hit the road

Blog Post

Education

TL;DR: Filing a motorcycle insurance claim involves four key steps: ensure safety and call 911 if needed, document everything at the scene with photos and witness information, contact your insurance company within 24-48 hours, and work with an adjuster to assess damages. Most claims are processed within 7-90+ days, depending on complexity. New riders should keep their policy documents handy, understand their coverage limits, and never admit fault at the scene. With proper preparation and the right insurer like Roamly, the claims process can be straightforward and stress-free.

How Does the Motorcycle Insurance Claim Process Actually Work?

Filing a motorcycle insurance claim starts immediately after an incident and typically involves four main phases: incident response, documentation, claim filing, and resolution.

When you're involved in a motorcycle accident or your bike is damaged, stolen, or vandalized, your insurance claim becomes your financial lifeline. Unlike car insurance claims, motorcycle claims often involve unique factors like seasonal riding patterns, specialized equipment, and higher injury risks that can complicate the process.

The good news? Most reputable insurers have streamlined digital claim processes that make filing easier than ever. Understanding each phase helps you navigate confidently and avoid costly mistakes that could delay your claim or reduce your payout.

What Triggers a Motorcycle Insurance Claim?

Common scenarios include:

- Collision accidents with vehicles or objects

- Theft or vandalism

- Weather damage (hail, flooding, wind)

- Fire damage

- Collision with animals

- Single-vehicle accidents (dropping the bike, road hazards)

What Should You Do Immediately After a Motorcycle Accident?

Your first priority is safety. Move to a safe location if possible, call 911 for injuries or significant damage, and begin documenting the scene before anyone leaves.

The moments after an accident feel surreal. Your adrenaline is pumping, your bike might be scattered across the asphalt, and your mind is racing through a thousand thoughts. Take a deep breath. What you do in the next few minutes will significantly impact how smoothly your insurance claim unfolds.

Immediate Safety Steps

- Check for injuries - Both yourself and others involved (adrenaline can mask pain)

- Move to safety - Get out of traffic lanes if you can do so without risking further injury

- Call 911 - Always call for injuries, major damage, or if the accident blocks traffic

- Secure the scene - Turn on hazard lights, set up road flares, and help direct traffic if safe

Critical Documentation at the Scene

Now comes the crucial part that many riders overlook in the stress of the moment: documentation. Your phone becomes your most important tool here. Start photographing everything before vehicles are moved or the scene changes. You'll want:

- Wide shots of the overall accident scene and all vehicles involved

- Close-ups of specific damage to your bike and other vehicles

- Road conditions - potholes, oil spills, construction zones, skid marks

- Traffic signs and signals - especially if they're relevant to fault determination

- Weather conditions - consider screenshots from weather apps for timestamp

While you're gathering visual evidence, collect essential information from other drivers involved:

- Driver's license and insurance information for all parties

- Vehicle registration details

- Contact information for any witnesses

- Police report number and responding officer details (if applicable)

Pro tip from experienced riders: Use your phone's voice memo feature to record your immediate recollection of what happened while the details are fresh. Include the time, exact location, weather conditions, and your observations about the sequence of events. This timestamped record can be incredibly valuable weeks later when insurance adjusters are piecing together the story.

How Do You File Your Motorcycle Insurance Claim Step-by-Step?

Contact your insurance company within 24-48 hours of the incident, provide basic details over the phone, and follow up with documented evidence through their claims portal or app.

Once you're home and the immediate stress has subsided, it's time to start the official claims process. The golden rule here is speed—most insurers want to hear from you within 24 to 48 hours, and honestly, calling sooner rather than later works in your favor. When adjusters see that you're proactive and organized, it sets a positive tone for the entire process.

Step 1: Initial Contact (Within 24-48 Hours)

Most insurers offer 24/7 claim reporting through:

- Phone hotlines

- Mobile apps

- Online portals

- Text messaging systems

Have ready:

- Your policy number

- Date, time, and location of incident

- Basic description of what happened

- Police report number (if applicable)

- Contact information for other parties

The first call is about getting your claim started and receiving your claim number, which becomes your reference for all future communications.

Step 2: Formal Documentation Submission

The real work begins with formal documentation submission.

Your insurer will request:

- Completed claim forms - Usually available online

- Photos of damage - Multiple angles, close-ups of specific damage

- Police report - If filed (may take 3-7 days to become available)

- Medical records - For injury claims

- Repair estimates - From certified shops (if requested)

- Proof of ownership - Registration, title, purchase receipts for accessories

Step 3: Insurance Adjuster Assignment

Within a few business days, you'll be assigned an insurance adjuster who will:

- Review your submitted documentation

- Schedule an inspection (in-person or virtual)

- Coordinate with repair shops

- Evaluate medical claims (if applicable)

- Determine fault and coverage

Step 4: Damage Assessment and Settlement

The final phase involves damage assessment and settlement negotiations.

The adjuster will assess:

- Repair costs - Labor and parts from certified shops

- Total loss threshold - Usually 75-80% of the bike's actual cash value

- Diminished value - How an accident affects resale value

- Rental coverage - If included in your policy

- Personal property - Gear, accessories, cargo damaged in the incident

What Documentation Do You Need for Your Motorcycle Insurance Claim?

Successful claims require comprehensive documentation, including photos, police reports, repair estimates, medical records for injuries, and proof of ownership for custom parts or accessories.

Think of claim documentation like packing for a cross-country motorcycle trip; you want to be prepared for any scenario without carrying unnecessary weight. The difference is, with insurance claims, more documentation is almost always better than less.

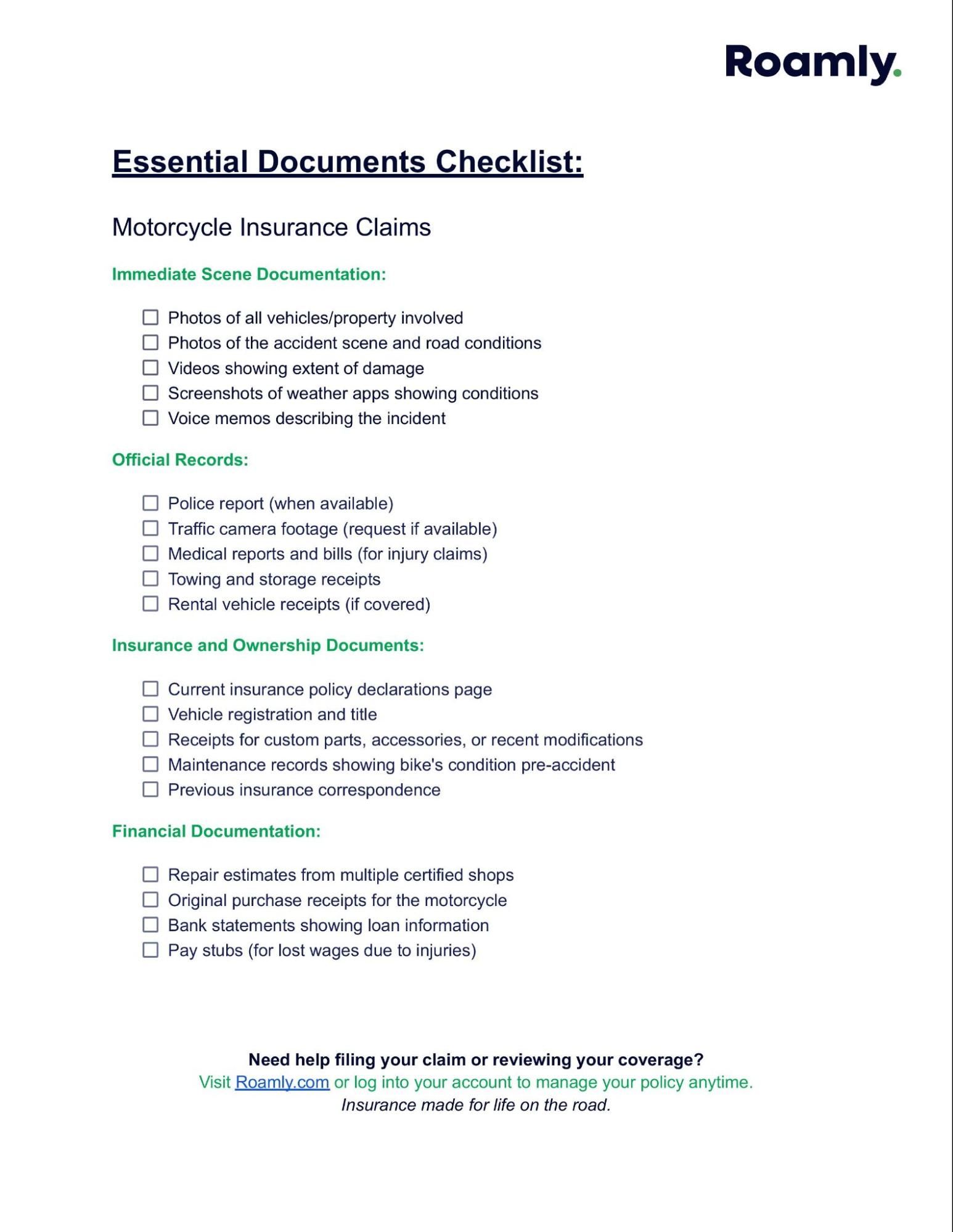

Download our “Essential Documents Checklist” to make sure you don't miss anything!

{kind=link}

Your immediate scene documentation forms the foundation of everything that follows. Those photos you took at the accident scene become the visual story of what happened, while videos can capture details that still photos might miss. If you managed to record a voice memo describing the incident, that contemporaneous account carries significant weight with adjusters.

Official records add credibility to your claim. The police report provides an independent account of the incident, while medical documentation proves the extent and cost of any injuries. Don't overlook seemingly minor expenses like towing fees; these receipts add up and should be covered under most policies.

Special Considerations for Custom Motorcycles

If your bike falls into the custom category, and let's be honest, most riders add at least some personal touches, additional documentation becomes essential:

- Receipts for all aftermarket parts and labor costs

- Photos showing modifications before the accident occurred

- Professional appraisals for high-value custom work

- Documentation proving modifications were reported to your insurer

Most importantly, ensure you've previously disclosed these modifications to your insurer, as undisclosed changes can complicate claims processing and potentially void coverage for custom components. For new riders considering their first bike purchase, understanding how modifications affect insurance is crucial. Check out our guide on the best motorcycles for beginners to learn about insurance considerations for different bike types.

How Long Does It Take to Process a Motorcycle Insurance Claim?

Simple claims with clear fault and minor damage are typically processed within 7-14 days, while complex claims involving major injuries, disputed liability, or total losses can take 30-90 days or longer.

The question every rider asks after filing a claim is: "When can I get back on the road?" The honest answer depends on several factors, but understanding typical timelines helps set realistic expectations and lets you plan accordingly.

Typical Processing Timelines

Minor Damage Claims (7-14 days):

- Single-vehicle accidents with clear circumstances

- Property damage under $5,000

- No injuries involved

- Complete documentation submitted promptly

- Clear fault determination

Moderate Claims (14-30 days):

- Multi-vehicle accidents requiring fault investigation

- Damage requiring multiple repair estimates or specialized parts

- Minor injuries with ongoing treatment

- Custom parts or accessories involved

- Weather-related delays in inspection scheduling

Complex Claims (30-90+ days):

- Serious injury claims requiring extensive medical evaluation

- Disputed fault situations need a thorough investigation

- Total loss determinations with valuation disputes

- Legal complications or attorney involvement

- Missing or incomplete documentation

Common Factors That Extend Processing Time

Several factors can either speed up or slow down your claim processing, and many are within your control:

- Documentation completeness - Missing photos, delayed police reports, or incomplete repair estimates

- Fault clarity - Accidents where responsibility requires investigation take longer

- Party cooperation - Unresponsive other drivers or witnesses can stall proceedings

- Injury complexity - Ongoing medical treatment naturally extends timelines

- Parts availability - Rare or discontinued motorcycle components can delay repairs

- Weather interference - Seasonal factors affecting inspection or repair scheduling

The good news is that most insurers now provide online claim tracking, so you can monitor progress and identify any bottlenecks that might be slowing things down. If your claim seems stalled, don't hesitate to contact your adjuster for a status update and clarification on what might be needed to move forward.

What Common Mistakes Should New Riders Avoid When Filing Claims?

The biggest mistakes include admitting fault at the scene, delaying claim filing, accepting the first settlement offer without review, and failing to document all damages including gear and accessories.

Every experienced rider has a story about learning something the hard way, and insurance claims are no exception. The mistakes that cost people the most money are often the ones that seem insignificant in the moment but have lasting consequences.

Critical Errors That Cost You Money

- Admitting Fault at the Scene: Never say "I'm sorry" or "It was my fault". Stick to factual observations only and let insurance companies and police determine fault. What feels like politeness can be used against you.

- Inadequate Documentation: Taking too few photos from limited angles and forgetting to photograph road conditions and signage. Not getting witness contact information or failing to document all damaged gear and accessories.

- Settlement Mistakes: Accepting the first offer without negotiation, not understanding your policy coverage limits, or settling before medical treatment is complete, and you understand the long-term implications. Don’t forget to also factor in the diminished value of your motorcycle.

- Communication Errors: Giving recorded statements without preparation, not keeping detailed records of all conversations, or failing to follow up on claim status regularly. Make sure to read all settlement documents carefully and keep a record of everything that happens (and is said) throughout the claims process.

Red Flags: When Your Insurer Isn't Playing Fair

Be cautious and consider seeking professional help if your insurer:

- Pressures you to settle quickly without adequate time for evaluation

- Refuses to explain coverage decisions or provide policy language

- Assigns fault without conducting a proper investigation

- Offers settlements significantly below repair estimates or market value

- Delays in communication or claim processing without a reasonable explanation

- Requests excessive documentation or repeatedly "loses" submitted materials

Communication throughout the claims process matters more than most people realize. Document every conversation with your insurance company, including the date, time, who you spoke with, and what was discussed. Follow up important phone conversations with email summaries. Read all settlement documents carefully before signing. Once you accept a settlement, you typically can't go back for additional compensation even if new issues arise.

How Much Will Your Motorcycle Insurance Claim Pay Out?

Claim payouts depend on your coverage types, policy limits, deductible amount, and whether your bike is repaired or declared a total loss, with actual cash value being the maximum for total losses.

Understanding what your claim might actually pay out requires decoding the sometimes confusing world of insurance coverage types. Think of your policy as a safety net with different sections designed to catch different types of financial falls.

Understanding Your Coverage Types

Liability Coverage:

- Covers damage you cause to other people and their property

- Required in most states with minimum coverage limits

- Won't help you repair your own motorcycle or cover your medical bills

- Choose limits based on your assets and potential exposure

Collision Coverage:

- Pays for repairs after accidents regardless of who's at fault

- Subject to your chosen deductible amount

- Covers up to your motorcycle's actual cash value

- Typically required if you're financing or leasing

Comprehensive Coverage:

- Protects against theft, vandalism, weather damage, and animal strikes

- Usually has a separate deductible from collision

- Covers "acts of nature" and criminal activity

- Essential protection for high-value motorcycles

Medical Payments/Personal Injury Protection:

- Covers your medical expenses regardless of fault

- Often includes lost wages and rehabilitation costs

- Has per-incident and per-person limits

- Provides immediate coverage while the fault is determined

Pro Tip: Recent research from the Insurance Institute for Highway Safety shows that motorcycles equipped with antilock braking systems (ABS) have 22% lower collision claim rates than identical models without ABS, which can translate to lower insurance premiums and fewer claims overall.

Total Loss Calculations and What They Mean

Your motorcycle is typically considered a total loss when:

- Repair costs exceed 75-80% of the actual cash value

- Frame damage makes safe repair impossible

- Airbag deployment (if equipped)

The actual cash value (ACV) calculation considers your bike's current market value minus depreciation and any previous damage. This isn't necessarily what you paid for the bike or what you think it's worth; it's what similar motorcycles are selling for in your local market at the time of the loss.

Gap Coverage Considerations: If you owe more on your loan than the actual cash value, gap insurance coverage can be a financial lifesaver by covering the difference. This situation is particularly common with new motorcycles that depreciate quickly in their first year.

When Should You Consider Hiring a Public Adjuster or Attorney?

Consider professional help for claims over $10,000, disputed fault situations, serious injuries, or when your insurer acts in bad faith by denying valid claims or delaying payments unreasonably.

Most motorcycle insurance claims can be handled successfully without bringing in outside professionals, but certain situations warrant considering additional expertise. The decision often comes down to complexity, claim value, and how your insurance company is treating you throughout the process.

Situations That Warrant Professional Help

Complex Injury Claims:

- Hospitalization, surgery, or long-term medical treatment required

- Permanent disability or ongoing rehabilitation needs

- Multiple medical providers and specialists are involved

- Lost wages that exceed your policy's medical coverage limits

- Disputes over the extent or cause of injuries

High-Value Property Damage:

- Custom or vintage motorcycles with specialized value

- Extensive aftermarket modifications or rare parts

- Disputed total loss valuations or repair cost estimates

- Multiple vehicles or properties are involved in the accident

- Claims exceeding $10,000 in total value

Insurance Company Problems:

- Claim denial without clear legal justification

- Settlement offers are significantly below fair market value

- Unreasonable delays in processing or communication

- Suspected bad faith practices or policy violations

- Complex liability disputes involving multiple parties

However, many claims can be successfully managed without outside help. Simple property damage claims with clear fault, single-vehicle accidents, most comprehensive claims like theft or weather damage, and situations where you have a good working relationship with a cooperative insurer typically don't require professional intervention.

The key is honestly assessing whether the potential additional recovery justifies the cost of professional representation. Public adjusters typically charge 10-15% of your settlement, while attorneys often work on contingency fees ranging from 25-40%. For smaller claims, these costs might outweigh the benefits, but for complex or high-value situations, professional expertise can often recover significantly more than you'd achieve on your own.

Get Back on the Road Faster with Roamly

Motorcycle insurance claims don't have to be overwhelming when you have the right support and coverage. Understanding the process, documenting everything properly, and working with a rider-focused insurer makes all the difference in getting back to what you love—exploring the open road.

Need help navigating your motorcycle insurance claim? Roamly makes it easy to file, manage, and get back on the road, faster. Our digital-first approach means faster claim processing, 24/7 mobile access, and support from advisors who actually understand motorcycle culture. Whether you're dealing with your first claim or want coverage that truly protects your riding lifestyle, we're here to help.

According to the National Highway Traffic Safety Administration, motorcycle riders are about 28 times more likely than passenger car occupants to die in a motor vehicle crash, making comprehensive insurance coverage and proper safety gear essential for every rider.

Get a quote or review your motorcycle coverage with Roamly today.

Disclaimer: This article provides general information about motorcycle insurance claims and should not be considered legal or financial advice. Insurance coverage varies by policy, state, and provider. Always consult your specific policy documents and speak with licensed professionals for advice about your particular situation.

Most insurance companies get a report from the Comprehensive Loss Underwriting Exchange (CLUE) to learn your claims history, even if the claim was with another company. Your claims follow you, but different insurers weigh them differently.

Coverage specifics (for gear, mods, rentals) always depend on the individual policy. Some insurers include gear and accessories up to certain limits, while others require separate coverage. Custom parts and equipment coverage is often available as an add-on for serious riders.

At-fault claims typically increase premiums at renewal, while not-at-fault claims generally don't affect rates. However, multiple claims of any type may impact your insurability. Premium increases vary by insurer, state, and your claims history.

If you have uninsured/underinsured motorist coverage, it will cover your damages. For hit-and-run accidents, comprehensive coverage may apply. Always file a police report immediately for uninsured or hit-and-run incidents.

Yes, you typically have the right to choose your repair facility, though your insurer may have preferred shops with guaranteed work and streamlined billing. Using preferred shops often speeds up the process, but isn't mandatory.

Most insurers require notification within 24-48 hours, though immediate reporting is recommended. Some policies specify "prompt" or "immediate" notification, which courts typically interpret as within a reasonable time frame given the circumstances.

Roamly Insurance Group, LLC ("Roamly") is a licensed general agent for affiliated and non-affiliated insurance companies. Roamly is licensed as an agency in all states in which products are offered. Roamly license numbers. Availability and qualification for coverage, terms, rates, and discounts may vary by jurisdiction. We do not in any way imply that the materials on the site or products are available in jurisdictions in which we are not licensed to do business or that we are soliciting business in any such jurisdiction. Coverage under your insurance policy is subject to the terms and conditions of that policy and is ultimately the decision of the buyer.

Policies provided by Roamly are underwritten by Spinnaker Insurance Company, Progressive Insurance Company, Liberty Mutual Insurance Company, Foremost Insurance Company, National General Insurance, Mobilitas Insurance Company, and others.

© 2026 Roamly All rights reserved.