May 12, 2026

The 2026 RV Insurance Market: Trends & Predictions

The 2026 RV Insurance Market: Trends & Predictions

K

By Kelly Lau

The 2026 RV insurance market is shifting. Here's what rising risks, stabilizing rates, and new trends mean for your coverage this year.

Insurance products

Blog Post

Education

TL;DR: RV insurance premiums are stabilizing for most owners in 2026 after two years of sharp increases. The national average auto premium fell 6% in 2025 and is forecast to rise just 1% in 2026. Wildfire exposure remains acute in the West, hail is a growing risk in the central U.S., and tariff-driven RV price increases are quietly raising insured values. Here's what it means for your coverage.

If you own an RV or you're shopping for one, it's a good time to understand what's going on in the insurance market. The last few years have been turbulent: premiums spiked, wildfires rewrote the rules in California, and a wave of new owners hit the road for the first time. Now, as we move through 2026, the market is shifting again and here's what the data says.

What Trends Are Shaping RV Insurance Right Now?

RV insurance in 2026 is being shaped by five forces: a growing and younger ownership base, a moderating rate environment, escalating weather-related risks, emerging telematics technology, and tariff-driven vehicle price increases. Each affecting what you pay and what you're covered for.

More RVers on the Road, and They're Younger

The RV market is growing steadily. Wholesale shipments hit 342,220 units in 2025, up 2.5% over 2024, and RVIA projects 349,300 units for 2026. Approximately 8.1 million U.S. households currently own an RV, and 16.9 million more have expressed interest in buying one within the next five years.

The median age of RV owners has dropped from 53 in 2021 to 49 in 2025, with first-time owners now making up 36% of all owners. Younger, first-time operators have statistically higher accident rates, a factor insurers weigh directly. Usage is also intensifying: median annual RV days jumped 50%, from 20 to 30, between 2021 and 2025. More miles, more campgrounds, more exposure.

Is the Rate Roller Coaster Finally Slowing Down?

If your premiums climbed sharply in 2022 or 2023, you weren't imagining it. Insurers were paying out more than they collected, triggering increases that pushed personal auto premiums up roughly 46% over two years. The correction arrived in 2025: the national average fell 6% to around $2,144, per Insurify's analysis of over 32 million rate quotes.

For 2026, S&P Global, Fitch, and Swiss Re agree that competition is intensifying and broad-based increases are unlikely for standard risks; Insurify projects with just 1% growth nationally. Full-time RVers, Class A owners, and anyone in wildfire-prone states will still see upward pressure.

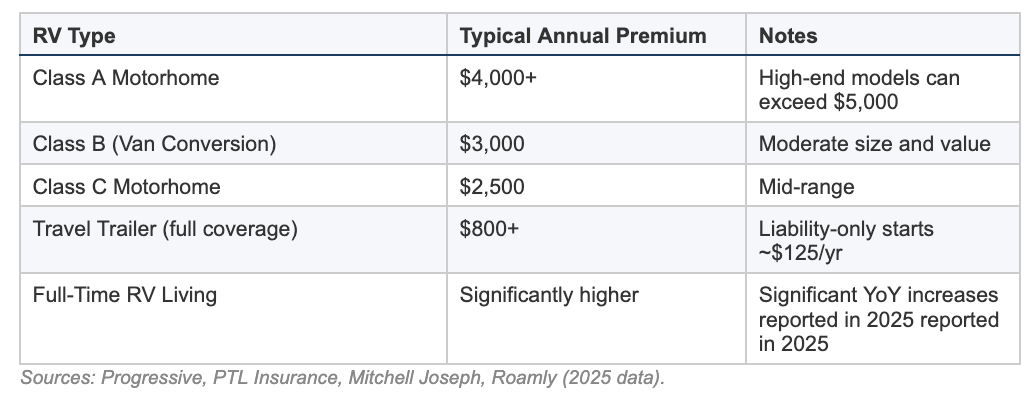

Typical Annual RV Insurance Premium Ranges (2025)

.

What Are the Biggest Risks Pushing Premiums Up?

Wildfire. The January 2025 LA wildfires generated roughly $40 billion in insured losses, the most expensive wildfire event on record, per Munich Re. California's FAIR Plan now carries $724 billion in total exposure, a 230% increase over recent years. For RV owners in California, Colorado, Oregon, and Washington: expect higher premiums and, in some areas, difficulty finding coverage at all.

Severe Weather. 2025 marked the third consecutive year U.S. severe convective storm losses exceeded $45 billion, per Moody's. RVs are especially vulnerable to hail, being large, flat-roofed vehicles with extensive glass surfaces. If you're in the central or southern U.S., comprehensive coverage isn't optional.

Vehicle Theft National vehicle theft fell 17% in 2024 to 850,708 units, the largest annual decline in 40 years, per the NICB and dropped another 23% in H1 2025. This is one of the factors enabling insurers to hold the line on rates.

Technology and Economic Forces

Telematics is gaining traction: usage-based insurance (UBI) rewards safe, low-mileage drivers with meaningful discounts. Meanwhile, tariffs on steel and aluminum have pushed 2026 RV prices up an estimated 3%–6%. Higher vehicle prices mean higher insured values and higher premiums, even without a rate change. The Fed held rates at 3.50%–3.75% as of January 2026; rate cuts would stimulate RV purchases and expand the insured market.

What Do These Trends Actually Mean for You?

For most recreational RV owners, 2026 brings pricing stability, but your situation matters. Where you live, how you use your RV, and what it costs to replace are the variables that determine whether your premium holds steady or climbs.

- Standard recreational user, good driving record: your premium is unlikely to jump. Rates have cooled and competition is increasing.

- Full-timers: expect continued pressure. Year-round exposure drives costs higher than recreational-use policies.

- Wildfire-prone states: don't assume your coverage auto-renews at the same terms. Review exclusions and check current availability.

- Newer or higher-value RV: your replacement cost has probably risen — check that your coverage limits reflect that.

- Hail country or flood-prone areas: comprehensive coverage remains non-negotiable.

What Will the RV Insurance Market Look Like Through 2026?

The consensus from rating agencies points to a more competitive market for standard risks — with continued pressure in wildfire zones and for high-value or full-time owners.

Premiums stabilize for most owners. Insurify projects roughly 1% growth nationally.

Wildfire exposure stays elevated. California's reform is underway, but stabilization is years away.

Severe weather is the most pervasive risk. Three consecutive years of $45+ billion in storm losses signal a structural shift, not an anomaly.

Insured values will rise even without rate increases. Tariff-driven price increases of 3%–6% mean your premium may tick up simply because your rig costs more to replace.

Telematics adoption accelerates. Low-mileage, safe-driving owners have a real avenue to lower costs, worth asking your insurer about.

The Bottom Line

The RV insurance market in 2026 is more nuanced than a single headline can capture. Rate increases are easing for most standard risks. But wildfire exposure is reshaping coverage availability in the West, severe weather keeps climbing the claims charts, and tariff-driven price increases are quietly pushing up insured values.

Treat your insurance like a tire check before a long trip: don't wait for something to go wrong to find out what you're covered for. Review your limits, understand your risks, and if something has changed; new rig, new location, full-timing now, make sure your coverage has kept pace.

Yes. Comprehensive coverage includes hail damage: dents, broken windows, and roof damage. It's especially important if you're in the central or southern U.S., where severe storm losses have exceeded $45 billion for three consecutive years.

UBI uses telematics: GPS and driving data to price your policy on actual behavior. Safe drivers with low annual mileage can qualify for meaningful discounts. Ask your insurer if a telematics program is available for your RV type.

If your RV was last appraised before tariff-driven price increases, your replacement cost may have risen 3%–6%. Review your limits and request an updated valuation from your insurer if needed.

For most recreational users, premiums should remain relatively flat, Insurify projects a 1% national average increase. Full-time RVers, wildfire-state owners, and Class A owners may still see upward pressure.

Full-time policies are underwritten like a hybrid of auto and homeowners insurance. Because your exposure to accidents, weather, and liability is year-round rather than seasonal, premiums are significantly higher than recreational-use policies.

Ready to make sure your coverage keeps pace with 2026?

Get a quote in minutes — and find out exactly what your rig is covered for.

Get Your QuoteInsurance terms, coverage, and discounts vary by jurisdiction. Reach out to us and we'll help you figure out what's right for your situation.

Sources

RVIA 2025 Annual Report; Go RVing/IPSOS 2025 RV Owner Demographic Profile; Insurify February 2026; Munich Re January 2026; NICB March 2025 & September 2025; S&P Global February 2026; Fitch Ratings January 2026; Intel Market Research December 2025; Triple-I/Milliman January 2026; Progressive, PTL Insurance, Mitchell Joseph (premium data).

Roamly Insurance Group, LLC ("Roamly") is a licensed general agent for affiliated and non-affiliated insurance companies. Roamly is licensed as an agency in all states in which products are offered. Roamly license numbers. Availability and qualification for coverage, terms, rates, and discounts may vary by jurisdiction. We do not in any way imply that the materials on the site or products are available in jurisdictions in which we are not licensed to do business or that we are soliciting business in any such jurisdiction. Coverage under your insurance policy is subject to the terms and conditions of that policy and is ultimately the decision of the buyer.

Policies provided by Roamly are underwritten by Spinnaker Insurance Company, Progressive Insurance Company, Liberty Mutual Insurance Company, Foremost Insurance Company, National General Insurance, Mobilitas Insurance Company, and others.

© 2026 Roamly All rights reserved.